Living off your nest egg is simple enough in theory: Switch to a portfolio focused on income and begin to withdraw your principal. How much of that principal you should withdraw, however, varies and may require some strategic thinking. Timing matters.

Money in, money out

Generally speaking, stock investments return 7-10% annually. Because of that, many people think they can withdraw 7-10% of their investments each year in retirement. In reality, that number is much lower:

For many of us, this can be a jarring realization. But there’s more to consider. To start, your portfolio is likely to fluctuate in value. If your portfolio balance is $500,000, a 4% withdrawal is about $20,000. The next year, a $20,000 withdrawal would be about 4.2% of your portfolio, if your principal remained the same.

Timing matters

When you’re building retirement savings, we talk about not trying to time the market: You can’t always buy low and sell high. But when it comes time to withdraw your money, market timing matters. If you have fixed living expenses in retirement, those expenses become a greater percentage of your nest egg each year, unless your portfolio continues to grow. Consider the same 20-year period in two different orders: At left, the down years happen early in retirement, and at right, they happen at the end.

This is a hypothetical example and is not representative of any specific situation. Your results will vary. The hypothetical rates of return used do not reflect the deduction of fees and charges inherent to investing.

These charts show actual returns for the S&P 500® from January 1, 2000, to December 31, 2019. The left side shows chronological order, the right side shows the period in reverse. Even though the average returns are the same, in one situation, you end up vastly better off.

The takeaway? Significant market downturns early on in retirement can have an outsized impact on your money and how long it will last. It’s still possible to retire successfully in a bear market, but the chart at left illustrates why it’s important for us to be more strategic about your withdrawals early on if the market is in a slump. For instance, we might lean more heavily on assets not tied to the stock market.

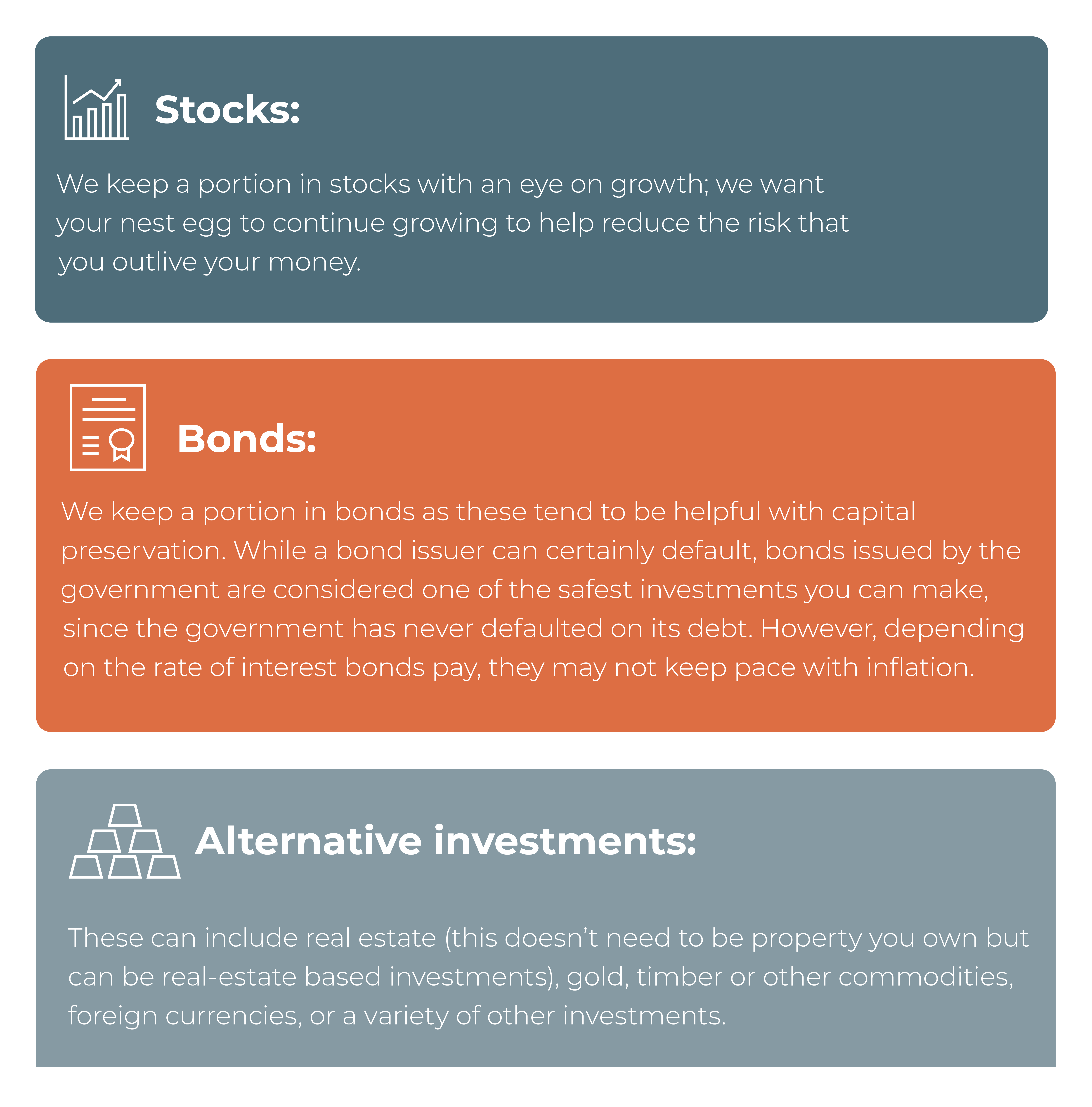

Portfolio considerations

The tables above look at an all-stock portfolio. But it would be incredibly rare for any retiree to have an all-stock portfolio.

When you’re invested in different types of assets, they tend to react differently to big market events. This can help protect you from the type of big downturns that can eat away at your retirement funds. This is particularly important early on.

Other considerations

If the market does experience a big dip early on in your retirement, we have other options. For instance, we can avoid withdrawing money from your retirement accounts when the value is lower by looking at alternate sources of income. These might include:

Ultimately, flexibility is the biggest factor in ensuring your money lasts through retirement. And we’re here to help with that. For instance, if the market hits a slump during your retirement, we may look for additional income streams for a few months so you can pause withdrawals and preserve your investments through that downturn. These are situations we monitor constantly on your behalf. If you have questions about the best way to handle income and spending in retirement, let’s discuss them at our next meeting.

All investing involves risk including loss of principal. No strategy assures success or protects against loss.